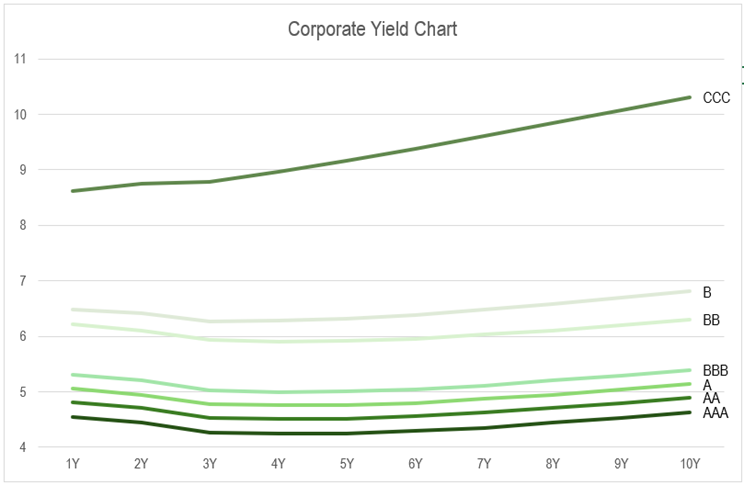

The impact of credit ratings on interest rates can be substantial. Interest rate spreads can vary significantly based on the issuer's credit rating. For example, the chart below shows the interquartile range (IQR) of yield-to-maturity for US$ denominated bonds as of November 26th, 2024.

In the transfer pricing context, subsidiary entities that borrow funds from a related party rarely have published credit ratings from credit rating agencies. In many cases, there may not even be a credit rating available for the ultimate parent entity of the borrowing subsidiary. While rating agencies publish shadow credit rating tools to assist with this analysis, these tools are often expensive and not specifically designed for transfer pricing applications. This practical limitation makes determining credit ratings difficult for many transactions. A good alternative for transfer pricing analyses is to use the Altman Z-Score model combined with historical benchmarking of Z-Scores by credit quality. This offers a defensible, data-driven approach to estimating creditworthiness for transfer pricing purposes. The advantage of this approach is that it provides an objective, quantitative framework that is:

- Well-documented in academic literature

- Based on publicly available financial data

- Cost-effective to implement