Rating agencies (like Moody's, S&P, and Fitch) offer proprietary solutions. These are good and reliable tools but have some drawbacks:

- They are a bit of a black box.

- Subscriptions to these proprietary models can be pretty expensive.

One alternative solution is the Z-Score model. Z-Scores have a proven track record. The Z-Score is built on simple ratio analysis. In the absence of better tools, the Z-Score provides a reasonable and systematic approach to help estimate the credit risk of a borrower in an intercompany financing transaction.

Below we summarize 3 practical ways in which the Z-Score can be used in the TP arena:

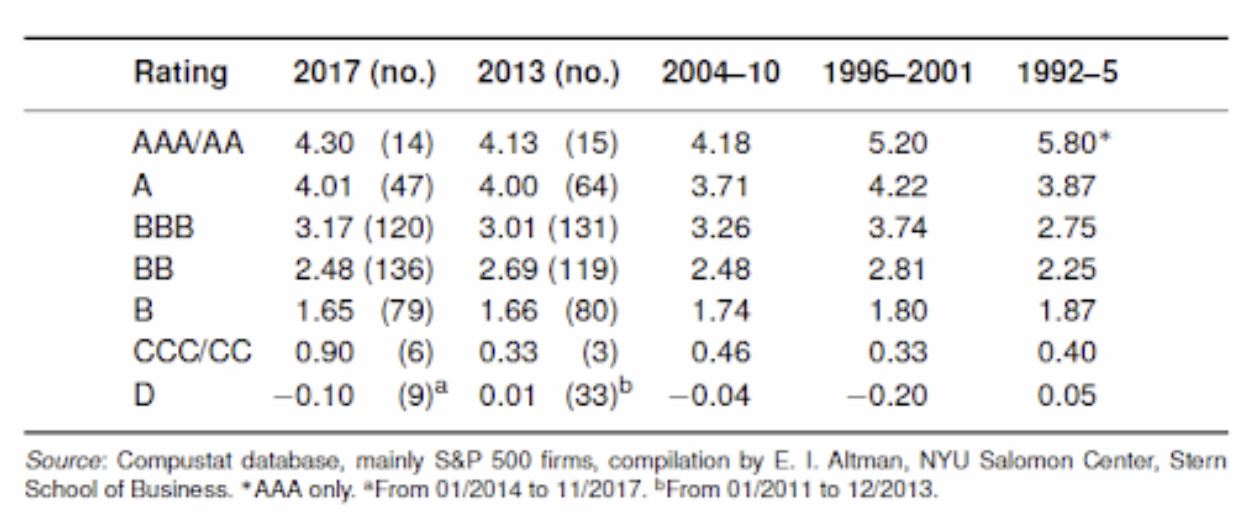

1) Map Z-Score to credit rating:

You can calculate your borrower's Z-Score and then map that to the Z-Score of rated entities. Ed Altman's 50-year retrospective does exactly this (see image below).

You can use this map (or an appropriately updated one for your loan) to help select the range of credit ratings you use in benchmarking for an arm's length interest rate. Keep in mind that Z-Scores were designed for US manufacturers, so you may need to customize them for your borrower's functions (more on that in #3).

2) Benchmark using the Z-Score:

You can forgo mapping to credit rating and simply search benchmark for arm's length interest using Z-Score. If your borrower's Z-Score is 2.5, you could consider searching for issuers (bonds, loans, or other appropriate debt instruments) that have a Z-score between 2.25 and 2.75.

3) Create your own score:

At its core, Z-Score is simply built of financial health indicators for US manufacturers. Based on the borrower's FAR profile, you can tweak to determine what are the best ratios for your intercompany financing transaction. You can then calculate your custom score on third-party issuer debt to help determine a benchmark for your specific situation.

Z-Score isn't a panacea for estimating credit risk, but it's a great starting point. It's certainly way better than the “thumb in the air” approach to determining creditworthiness that we have seen in the wild.